Tencent Music

China’s leading music streaming service? A comfortable hold amidst the AI hype.

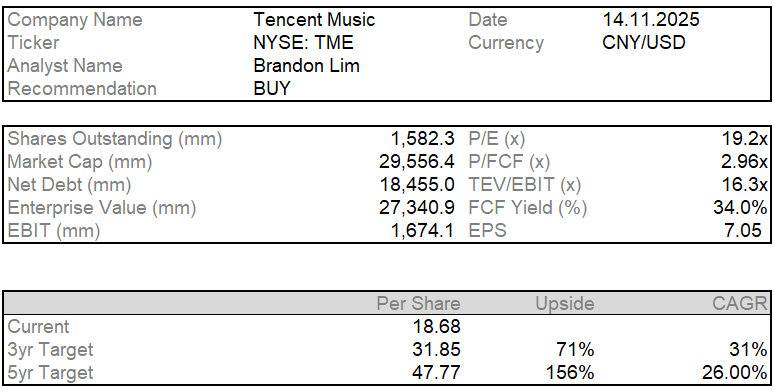

Table for my club’s purposes, anyway, my 1Y price target stands at USD 20.9, implying an 11.7% upside.

Tencent Music (NYSE: TME) is the leading music streaming service provider in China with over 70% market share. It operates a repertoire of apps – QQ Music (it’s flagship app), Kugou Music, Kuwo Music and WeSing. Previously predominantly social entertainment, TME now has the bulk of their revenues from online music services at ~75%+ of total revenue.

Core thesis points I will consider on why it is an attractive to buy despite the rally this year is because (1) industry tailwinds in the Chinese consumer sector, continue to drive penetration in online music services (2) TME is able to effectively monetize its consumers and its efforts are starting to bear fruit these quarters

Currently, TME has pivoted from subs-at-all-cost to (1) monetization (2) ARPU uplift and finally (3) user quality

From reading multiple reports, it seems that the street is mainly pricing in ARPU uplifts coming from SVIP and decreasing promos (hence decreasing cost of revenue/increasing topline)

Anyway, the question remains if churn is high since TME is pivoting away from this subscriber at all cost model

Perhaps Ximalaya deal has not been fully priced in the long run.

P.S. apologies for the lack of chart/visuals, I am emulating a wise writer/investor/PM that just rambles his pitches quickly (tbvh I am still experimenting what works, visuals can come later)

Industry: The industry leader in a market where paying for music is still somewhat nascent

The music industry in China is interesting, insofar that (1) Despite large adoption of online music, penetration of paid music lags that of the West (~11% vs ~52%) (2) “Fans economy” in China is huge at about US$170bn (~15% YoY). Therefore, live streaming/concerts could be the next leg up as a key strategy in monetizing the consumer.

TME is an early beneficiary to this with their exclusive licensing, allowing them to capture a huge chunk of the market share. However, this was back in the heydays as the government has clamped down on said exclusivity. However, I still hear from users that TME still has a better library of music vis-à-vis peers. Will explore this point below!

A fragmented music industry, high bargaining power on the supply side favouring TME: China’s rights landscape is fragmented with majors, local labels, and indie aggregators all negotiating bilaterally. Tencent Music’s early mover in establishing a ~70% market share gives it bargaining leverage, allowing it to lock in fixed-fee or hybrid licensing deals that cap marginal cost growth as usage scales. Because much of consumption is Chinese-language repertoire from local partners or TME’s own production, royalty rates are materially lower than Western benchmarks — in some cases less than half per track.

Favourable unit economics: For global majors (UMG, Sony, Warner), TME’s long-standing relationship with them allows for favourable terms that see minimum-guarantee pricing structures rather than the more expensive pure per-stream rates that Spotify has. I would attribute this to China being incremental revenue and not a core market, and they are willing to accept this in exchange for distribution into TME’s massive user base. This structural cost advantage underpins TME’s margin resilience compared to the higher licensing constraints faced by Spotify (FY20-FY24 GM: 26.7% vs TME’s 34.1%) with Spotify paying 65-70% of its revenues as royalties.

Supply: Chinese consumers rarely paid for recorded music due to entrenched piracy, paid streaming penetration only stood at 11% of the current population. However, assessing the overall streaming industry, it is great to see MAUs of Netease and TME growing, as well as their paying ratio, indicating the increasing monetization of customers. As customers are increasing more willing to pay for music streaming services, I shall elaborate, very briefly, what makes a customer pay and eventually stay (thereby increasing its lifetime value) – of which TME leads the industry in.

Content Access: TME has multi-year renewals with UMG (2024), Sony (2025), Warner, plus strong domestic label coverage. Furthermore, TME’s expansion into long-form content is strategic in which I believe follows Spotify’s footsteps given the success the latter has seen driving further topline

Product – ecosystem, usability and value for money: Deep integration with Tencent ecosystem through WeChat login and pay. This allows for low-friction and sticky integration into existing social habits, reducing churn. Furthermore, TME charges roughly RMB 10-12/month across its apps and RMB 30-40 for SVIPs.

Unique perks – durable growth drivers to the business: This portion is where I believe TME stands out the most ahead of its competitors. Given its early-mover in the market, TME now enjoys the luxury of monetizing existing customers rather than growing its customer base. Its scale further allows it to think more on how they could get customers to spend more and bring unique experiences only achievable due to their scale. This essentially moves TME from being “just a music streaming platform” to a fan identity platform – one which has a cult following since it leverages on positive experiences

Yet the threat of entrants cannot be understated. It is true that TME has lagged in terms of DAU/MAU compared to Soda Music (ByteDance – I blame douyin for being too good at capturing the attention and brainrot of my generation), with Soda music capturing more user time spent as well.

Tencent Music’s Ecosystem:

Creating a strong fanbase via bundling: These are just the initiatives management has created to further entice users to stay in the TME ecosystem. They all fall under a “bundle service” for SVIP – basically more reason to upgrade.

Bubble: An app that gives fans the feelings of private direct interaction with K-pop idols. Management has also stated that they plan on introducing Chinese artists into the bubble community and are adding features such as live streaming.

Stake in SM entertainment: May 2025, ~9.7% stake, gives TME more influence in content, promotion and more importantly, preferential access to SM artists’ content (see SVIPs’ priority access to G-Dragon’s concert and Blackpink’s concert pass).

Finally, merchandising and the offline economy: Management has discussed increasing the role of merchandise especially with revenue from concerts, merch and artist related services having more than doubled y/y. TME also plans to announce an annual membership card tied to shopping malls/merch to offer further discounts on physical merchandise.

There are two cases which are interesting to consider in this business which I will discuss here – SVIPs and TME’s ecosystem as a durable advantage – both of which relies heavily on the consumer. Given that management and the street narrative are mostly focused on TME’s monetization growth, diving into these factors are well-worth a discussion.

Is this SVIP strategy really a durable growth driver that management claims?

We are currently now at roughly 7+ consecutive quarters of ARPU growth and about 4 consecutive quarters of management’s explicit attribution to SVIP (this consistent ARPU growth is clearly reflected in the ~97% YTD performance as of the time of writing). Clearly the street is optimistic on management’s strategy.

Let’s take a look at what SVIP is.

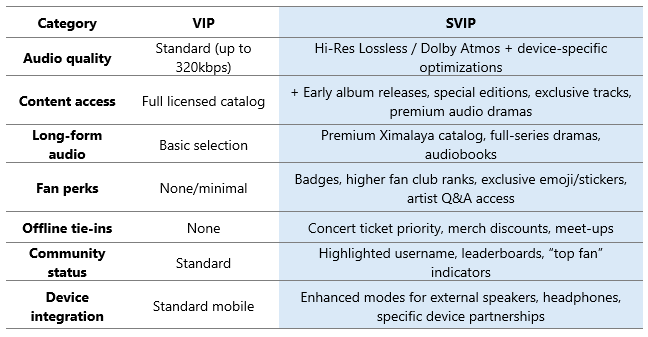

SVIP is TME’s premium-tier subscription, positioned above the standard VIP (costing 3x more). SVIPs enjoy a bundle of audio quality, exclusive content, fan perks, and community features. Uniquely, this does not really work in the West as users expect near-complete catalog parity across platforms. Bundling perks doesn’t replace catalog access – and the intangible experiences do matter more to Chinese consumers.

Management has emphasized repeatedly on SVIPs being a durable growth driver to the business with premium sound quality (surprisingly to me) being the most popular SVIP membership benefit. Additionally, artist-centric privileges have become effective at boosting SVIP adoptions – speaking from personal experience, I have seen friends who are willing to pay $8 a month just to be in an exclusive chat with idols. SVIP members have grown from 10M in 3Q24 to 15M in 2Q25 now standing at roughly.

Surely enough, this ARPU-driven growth strategy has been working out for management – ARPPU has been trending upwards at about ~10-15% YoY growth, steadily increasing towards 11.9 in 3Q25.

How durable is SVIP as a growth strategy?

Prima facie, SVIP is quite a smart play by management.

Paying ratio and ARPU is healthy, ARPPU has room to grow at ~12

More partnerships with companies TME takes a stake in which continue to bring in benefits from fans keeping the engagement higher

…at least until other players (Netease/Soda) disrupt. Could there be a bear case on this strategy.

For starters, TME’s user time spent continued to decline in 2Q25 while Soda music and Netease music outperformed TME. Could TME lose its non-paying music base faster? Perhaps. I do think there is merit for Soda Music to gain more of the market share given how virtually every youth uses Douyin in China (~760M MAU).

Music and short-form video go hand-in-hand. We have seen the resurgence of old songs blowing up in the charts on Tiktok (see old-school classics rising in popularity). With the youth spending more time on short-form videos (self-explanatory), I do think that a company which is able to cause this seamless synchronization between app -> music will be the cherry on top to retaining the next generation of music listeners

So what’s stopping Soda Music/Netease from capturing more share? How much of a lock-in does Tencent Music have? How much of a pull factor are fan benefits and TME’s early mover?

To understand the consumer…

Consumers are price sensitive, but there is friction in porting over their music library. That’s what makes Spotify successful till this day, combining the social (Spotify wrapped) with access to a huge music catalogue (there is already near complete library parity across the different platforms). Once you have built your whole library on the platform, it is hard to leave (your playlists, shared songs, recommendation algorithms). You get fomo when your friend posts their Spotify Wrapped and create shared playlists and albums. It is a hassle to change from one platform to another while you are paying roughly the same price across platforms.

Notably in China, streaming services have yet to reach the level of music catalogue parity. While exclusivity has been removed and NCM is catching up with their deals with various labels such as Sony, Kakao Entertainment, CJ Entertainment etc, TME still boasts the largest catalogue of music at ~260M compared to NCM’s ~150M.

Major labels currently only represent ~20% of Chinese consumption, making domestic/Kpop relationships more important. It seems that NCM is catching up on its catalogue in domestic labels too (Rock Records renewal, UMG licensing agreement,

While Soda Music is still new, there is a possibility they will catch up in catalogue access as well given their growth in users. Yet, ARPU and paying user growth in TME does support my point that switching is not particularly common amongst the consumers. Until we see a hit in paying ratio, I’ll give the competition scenario higher merit.

Therein lies the reason why TME is focusing on monetizing the fanbase so much and focusing on the social aspect that Spotify excels in. Perhaps the lock in of the consumer now lies in offline experiences… can TME achieve this?

Pivoting to concerts, assessing the fans economy as a whole…

Priority access to ticket purchases for in-demand concerts. G- Dragon and Blackpink priority access tickets, “online concert high-definition viewing rights”

This is something NCM lacks given the lack of focus on building this Fans economy compared to TME.

Management cited concert-related privileges and artist engagement as strong catalysts for SVIP sign-ups. TME reported that bundling digital albums and concert ticket privileges with SVIP increased conversions significantly.

Fans economy is huge in China. Chinese consumers contribute to ~30% of many Kpop group’s digital sales, BTS, Blackpink, Twice etc frequently chart on QQ Music and NCM’s lists. TME-held G Dragon’s concert sold out on three consecutive days in Macau and facilitated ~100+ offline concerts in the first half of 2025.

While it is rather hard for me to quantify the exact contribution to total revenue of offline concerts and merchandising, it is pretty much clear that the fans economy is here to stay. I’ll just have to take management’s words in saying fans economy and live events revenues are increasing faster than the gross margin hit from building this. After all, more exclusive live events = more signups for SVIP for the exclusive perks (speaking from personal experience, I would pay more just to avoid the hell which is queuing on ticketmaster for hours and seeing the man walking in the queue but never seems to move forward) = larger ecosystem overall == flywheel!

Assessing the XML deal

Management states that they are still waiting on regulatory approval for the XML deal and hence are unable to provide many details. But the gist of it is that in acquiring XML for ~$2.4bn, TME will directly have acquired the 300+M MAUs on the platform, onboarding more unique listeners and cross-selling synergies.

Given that the deal is still in the works, there is a chance that this is not fully priced in, so let’s educate ourselves more on the potential of this acquisition.

Firstly, the saga of Spotify and podcasts. Spotify made ~$1bn worth of investments in acquisitions and content deals as part of their “Audio-First” Mission back in 2019.

Exclusivity strategy failed – Joe Rogan’s podcast was made public again after Spotify realized they could monetize better through exclusive ads instead

Podcast revenue showed promising growth but was still tiny relative to total revenue (est $190M podcast rev in 2022 vs $17bn total revenue)

Perhaps podcasts provided a larger library and indirectly justified Spotify to raise prices. Coupled with cost cuts, they finally turned profitable in 2024.

Hence, arguably mixed results from Spotify’s podcast shift.

Is this time different?

Do Chinese consumers listen to podcasts? Yes. The long form audio industry is estimated to reach ~RMB 30bn with a unique user base of ~520m. Of this, XML has 300m MAU and 12% paying ratio at an ARPU at RMB 13.4 (notably higher than TME).

From a business standpoint, I do think it is a great move for management to integrate XML into the platform given that penetration of paying users for podcasts has room to run vs in the West. Furthermore, TME’s long-form audio content is admittedly weak, hence why try to grow it organically when you can acquire the largest player and cross sell to your user base from there.

“This time is different”. There is a case to be made that XML is complementary to the different membership tiers that TME has compared to Spotify. For instance, the free members could be on ads-based listening, green diamond/VIP members could have access to more premium catalogue and SVIP members could have access to the entire package as part of the bundle. This is a flexibility that Spotify did not have and TME does not have to chase for exclusivity in podcasts when they are already acquiring the largest podcast distribution platform.

This could drive margins higher. Just like what Spotify has done incorporating ads > exclusive distribution, TME’s advertising revenue should similarly see an increase as user time spent increases across the board. Also, worth to note ~10-20% shared audience of both TME and XML, interesting to see the cross-selling dynamics and lower CAC here.

Thoughts, uncertainties and valuation

There are a few uncertainties and overhang…

Just nicely at the time of this writing TME’s 3Q earnings are out, and the stock has sold off -10%. I was initially going to write this off as a comfortable hold, but these levels give a greater sense of comfort.

An RMB 8.46bn revenue in Q3, 20.6% YoY, +2.8% above cons. EPS came in at 1.54, 1.5% above cons. Monthly ARPPU continues to increase to 11.9 from 10.8, gross margins up 90bps YoY to 43.5%. I was right that the stock has been priced to somewhat perfection before this quarter’s print, but a 10% selloff right after seems quite an irrational reaction to me.

It does seem that the street is extremely worried about competitive pressures as multiple analysts asked about competition as peers are gaining MAU (particularly Soda Music). Weird point to me…if anything they should have known about it quarters ago where this bunch of analysts were equally bullish about management’s SVIP strategy. Also, gross margin hit reiterated by management due to new initiatives of building the fans economy…but again, nothing new.

Mitigations…

I don’t foresee users fleeing to other platforms when they have built their playlists around this ecosystem at reasonable price vs peers as we have discussed earlier. Management’s vague answer on dealing with competition through their huge catalogue is actually true, I believe the consumer will only switch when (1) price is too high or (2) no music from their favourite artist.

Perhaps the bulk of the listeners that contribute to the decline of MAU comes from the free/lower tiers and TME is able to retain and monetize their more “valuable” customers. As long as ARPU does not see a significant hit, I believe we are good to go.

More clarity of the XML deal in the near term could prove to be a catalyst as we’ll finally see the long-awaited synergies that management has promised, along with concrete plans they have for the platform.

Finally, valuation and assumptions…

Not a fan of DCFs, hence valued TME on a forward P/E approach relative to music peers. At 22.2x forward median P/E across music peers, I arrived at a 1Y TP of US $20.9 for TME (implying a 11.7% upside). I am sure there is room to argue that you could assign a higher multiple considering Spotify trades at ~49x but I am inclined to be more conservative in my projections to reflect (1) near term competition risk depressing the stock price (thus shows the irrationality of the sell-off) and (2) low volatility of this name suggests longer reversion to the upside, I am big on opportunity cost in this “AI supercycle”.

List of notable assumptions:

- 27 revenues projected to price in XML deal, but it’s yet to be reflected in my 1Y target price (why price this in if we are looking in a year where markets are crazy and you may very well pay for the opportunity cost of holding this when semis/AI are exploding).

- Paying ratio to trend upwards towards 25%+ in 2027, in line with street estimates (current 3Q paying ratio: 24.2%). SVIP % of paying users continue to trend upwards towards the high 30s from 2027 onwards (such is a byproduct of declining MAUs, higher paying ratio and higher SVIP penetration).

- Tapered YoY growth from 27 as I believe SVIP growth matures as a strategy albeit the uplift from XML. Well of course if I further projected 3-5 years, theoretically it would imply a way higher price target, but too many assumptions will be baked in and I am not comfortable with these “bubble” conditions we are in to be so optimistic in my views and spout 3-5 year price targets.

Final thoughts:

I do think TME is well-positioned and management is extremely strategic in creating an experience for fans while the rest of the industry catches up on music catalogue.

I am still quite certain intuitively that consumers will not easily switch to another platform once they have built their entire playlists on TME.

Only time will tell if all the bundled benefits (concerts, merchandising, XML) will prove effective in driving SVIP higher. The moment ARPU takes a hit and competitors actually catch up

Case of price war? I don’t really foresee it happening as consumers have demonstrated the willingness to spend more for incremental benefits and frankly, NCM/Soda still have to ensure they can pay the artists so you’ll have to keep membership prices level.

So, yes TME is a comfortable hold at these levels. Clarity on XML is still the one thing I feel is necessary as the next driver of this bundled SVIP strategy. ARPU, paying ratio are all far more important metrics than MAU growth (of course, barring a huge decline in MAU).